Active fund managers continue to fight a losing battle

Active fund managers continue to fight a losing battle

Most active managers fail to beat the market yet customers still pay high fees

When you pay someone to do a job for you, if they fail to do it properly you can usually get them to put things right or get some or all of your money back. When it comes to the active fund management industry this does not apply.

For years, active fund managers have asked customers to give them money so that they can use it to beat the returns of the stock market. They say they can do this because they have some form of edge or process to find winning shares and avoid losing ones.

In return for doing this, they will skim off a bit of the value of your portfolio each year as a fee.

There are some very talented fund managers out there who have made good on this promise but the vast majority of them fail to do so.

This is not because they are lazy or incompetent, it is because beating the market is very hard to do.

The Top 5 Performing UK Fund Managers over 5 Years

Source: Citywire 31/1/19 t0 31/1/24

In very simple terms, not all managers can beat the market because together they are the market. Not everyone can be above average at doing something - there has to be some winners and losers.

This week, I read a Morningstar article citing data from S&P Dow Jones Indices which said that the vast majority of US large company equity funds had failed to beat the S&P 500 for the 14th consecutive year.

I’m not too surprised as the S&P 500 is a notoriously hard index to beat, especially in recent times when its value has been driven by just a few big technology stocks.

So I decided to look at how UK fund managers have been performing.

I’ve had conversations with a few private investors in the past who reckon that the FTSE All Share index is easy to beat because it’s full of bad companies, or big mature companies that find it hard to grow. If you just avoid these, you’ll beat the market.

Well, if this is true - and I don’t believe it’s as simple as this - then professional fund managers don’t seem to be following this strategy.

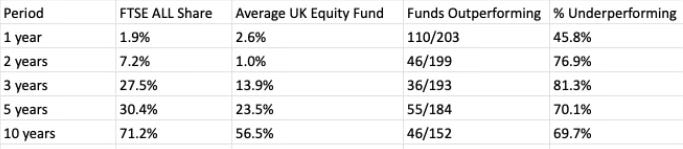

Over the last decade, the average UK All Companies Fund has failed to beat the FTSE All Share index. A rare exception was last year when a small majority did. That said, the benchmark was very low and could have been beaten by sticking money in a savings account.

Source:Citywire/SharePad: Data to 31st January 2024

Looking beyond one year, the statistics do not make for pretty reading. Around 70-80% of UK All Companies Funds still in existence (many bad ones have been wound down or merged into other funds) have failed to beat the market.

Performance of UK All Companies Funds

Source: SharePad/Citywire Data to 31st January 2024

Even fund managers whose names regularly appear in the financial media have underperformed over five years. Nick Train has returned 29.2% while Keith Ashworth-Lord has returned just 13.3%.

Global fund managers such as Terry Smith have also underperformed. His five year return has been 72.7% whereas an iShares MSCI World ETF has returned 79% to UK investors and the iShares S&P 500 96.8% according to SharePad.

In some cases, these managers have been - and continue to be - paid very large sums of money. This is often the result of performing very well in the past and attracting large sums of money to manage.

In turn, the bigger their funds get, the harder it becomes to deliver meaningful outperformance. However, the fund managers are still getting paid large sums for just having lots of money to manage rather than beating the market.

Investors are of course free to take their money elsewhere and many have chosen to do so. Yet, there is no compensation for underperformance or rarely any benefits from lower fees as the fund has got bigger.

In other industries and markets, customers have some redress if the product or service they buy doesn’t live up to expectations. Economies of scale often lead to lower prices.

Exchange traded funds (ETFS) have made it very cheap and easy for investors to capture the returns of hot markets and build portfolios to suit their needs and they have become the active fund management industry’s biggest threat.

Many of you reading this will have decided to look after your own money and I don’t blame you for doing that.

I also have some sympathy with professional fund managers. They operate under lots of constraints which makes their job more difficult.

That said, the business model is badly broken and needs fixing. It starts with having a fee structure that properly and fairly aligns their interests with their customers’ while reflecting the difficulties of beating the stock market.

My thoughts on how to do this will be left for another time.