Reckitt Benckiser: A falling knife you may not want to catch

Reckitt Benckiser: A falling knife you may not want to catch

Litigation liabilities are unknown but could be big. Shares could stay cheap and get cheaper

Reckitt Benckiser (“Reckitt”) has not been having an easy time of late. Its products and shares were once lauded as a dependable consumer staple that investors could rely on for steady growth.

This has not been true for some time. In fact, Reckitt and its peers such as Unilever have been struggling to get consumers to buy more of their products. Volume growth - in other words real growth - has been hard to come by.

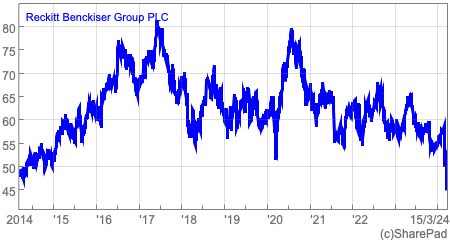

Without sustainable growth, the case for buying its shares is a weak one. The lack of growth has been the chief reason its shares have been such poor performers.

Total returns have been a meagre 25% over the last decade compared to 71% for the FTSE All Share Index. US giant Procter & Gamble’s shares are up by 140% over the same period.

You can look at Reckitt’s portfolio of brands such as Finish, Dettol, Nurofen, Durex, Gaviscon and Vanish and think that they have a lot to offer. They do, but much of what Reckitt sells is increasingly vulnerable to private label products that are getting better in quality and are sold for a much lower price.

Going forward, Reckitt’s annual revenue growth is expected to be an unspectacular 3-4% with earnings per share (EPS) being juiced up by cutting costs and share buybacks. This is not a pitch that is likely to get too many investors excited.

Last Friday (15th March) saw the kind of news shareholders dread. Reckitt has lost a lawsuit in Illinois, US. A judge awarded damages of $60m against the company in a case where it has been alleged that its baby milk products caused the death of a child. Reckitt continues to dispute this.

Despite this being an isolated case, investors clearly think that a precedent may have been set for more to follow and over £5bn was wiped off the market value of the company.

Diligent readers of company reports will have been aware of the lawsuits in the contingent liabilities note to Reckitt’s 2023 results. Even if they had read it, they would have been told that they should not really worry about it too much:

Necrotizing Enterocolitis (NEC)

Product liability actions relating to NEC have been filed against the Group, or against the Group and Abbott Laboratories, in state and federal courts in the United States. The actions allege injuries relating to NEC in preterm infants. Plaintiffs contend that human milk fortifiers (HMF) and preterm formulas containing bovine-derived ingredients cause NEC, and that preterm infants should receive a diet of exclusive breast milk. The Company has denied the material allegations of the claims. It contends that its products provide critical tools to expert neonatologists for the nutritional management of preterm infants for whom human milk, by itself, is not nutritionally sufficient. The products are used under the supervision of medical doctors. Any potential costs relating to these actions are not considered probable and cannot be reliably estimated at the current time.

Source:Reckitt Benckiser 2023 Annual Results statements

In response to the ruling, Reckitt is trying to calm investors by saying:

“It is important to note that this is a single verdict in a single case and should not be extrapolated.”

This advice has been ignored, which is understandable given that the company’s previous view on the matter has been challenged.

Health issues from products should not be trivialised and there is clearly a serious issue facing the company here. It’s not difficult to extrapolate this case to a situation where thousands seek compensation and the bill runs into billions of dollars.

Reckitt is now in a very vulnerable situation, and the fall in its share price will surely have piqued the interest of contrarian investors.

The shares are at a ten year low at 4486p and trade on just 13.5 times the next year’s forecast EPS. This compares with Unilever on just over 16 times and US peers Procter & Gamble and Colgate Palmolive on around 24 times.

Reckitt’s much lower valuation is bound to spark takeover chatter and there will be no shortage of investment bankers that would love to make a deal happen.

That said, the clouds hanging over the company are big and could take a long time to clear. This makes the shares a falling knife that you may not want to catch.